When shopping for a home, securing mortgage pre-approval is one of the most important steps you can take. Not only does it show sellers that you are a serious buyer, but it also gives you a clearer picture of your budget and financing options. However, many homebuyers do not realize that mortgage pre-approval can be leveraged in multiple ways to maximize their home search and negotiation power.

When shopping for a home, securing mortgage pre-approval is one of the most important steps you can take. Not only does it show sellers that you are a serious buyer, but it also gives you a clearer picture of your budget and financing options. However, many homebuyers do not realize that mortgage pre-approval can be leveraged in multiple ways to maximize their home search and negotiation power.

Strengthen Your Offer in a Competitive Market

In today’s fast-moving real estate market, multiple offers are common, and homes sell quickly. Having a mortgage pre-approval letter in hand can set you apart from other buyers. Sellers are more likely to accept offers from buyers who have already secured financing since it reduces the risk of the deal falling through due to financial issues.

Gain a Competitive Edge in Negotiations

A strong pre-approval not only makes you an attractive buyer but also gives you leverage during negotiations. Sellers may be more willing to accept a lower offer if they know the financing is already in place, reducing delays and uncertainty.

Identify Your True Budget

Pre-approval helps you determine the maximum loan amount a lender is willing to offer, but that does not mean you should borrow up to that limit. By knowing your approved amount, you can confidently search for homes that fit within your comfort zone without overspending.

Speed Up the Closing Process

A mortgage pre-approval means much of the underwriting process has already been completed, allowing you to close on your new home faster. This can be a significant advantage if you are in a time-sensitive situation, such as relocating for a job or moving before your current lease expires.

Show Confidence to Real Estate Agents

Agents take pre-approved buyers more seriously because it signals that you are ready to move forward with a purchase. This means you will receive more attention, better service, and access to homes that match your financial qualifications.

Secure Better Loan Terms

Getting pre-approved gives you a chance to compare different lenders and loan options before committing. This allows you to shop for the best interest rates, down payment requirements, and loan terms, ensuring you get the most favorable deal.

Avoid Last-Minute Surprises

Without pre-approval, buyers sometimes fall in love with homes they later find out they cannot afford. Pre-approval prevents this by setting clear expectations upfront, avoiding heartbreak and wasted time.

Mortgage pre-approval is not just a box to check, it is a powerful tool that can give you an advantage throughout your home-buying journey. From making stronger offers to negotiating better terms, using your pre-approval strategically can make all the difference.

If you are ready to start house hunting, let’s connect. I can guide you through the pre-approval process and help you make the most of your mortgage options.

Buying a home in a remote area can be a dream come true—peaceful surroundings, open spaces, and a slower pace of life. However, securing a mortgage for these properties comes with unique challenges. As a mortgage originator, I’m here to break down the hurdles and offer solutions so you can make your rural homeownership dreams a reality.

Buying a home in a remote area can be a dream come true—peaceful surroundings, open spaces, and a slower pace of life. However, securing a mortgage for these properties comes with unique challenges. As a mortgage originator, I’m here to break down the hurdles and offer solutions so you can make your rural homeownership dreams a reality.

If you’ve been managing your finances responsibly but don’t have a traditional credit score, you may be wondering whether homeownership is still within reach. The good news? It is! While most mortgage lenders rely on credit scores to assess your creditworthiness, alternative credit history—like rent payments, utility bills, and other recurring expenses—can help you qualify for a mortgage.

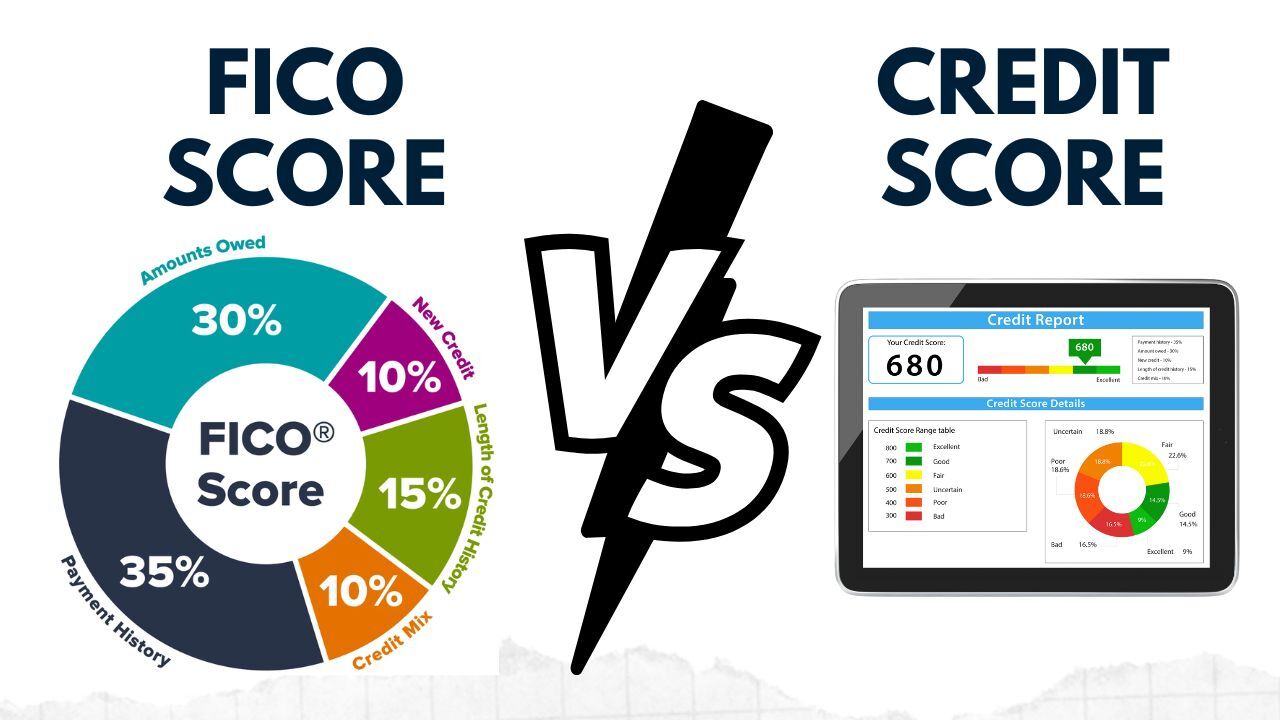

If you’ve been managing your finances responsibly but don’t have a traditional credit score, you may be wondering whether homeownership is still within reach. The good news? It is! While most mortgage lenders rely on credit scores to assess your creditworthiness, alternative credit history—like rent payments, utility bills, and other recurring expenses—can help you qualify for a mortgage. When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences.

When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences. Securing a mortgage as a self-employed professional can be more challenging than for traditional W-2 employees, but with the right preparation and documentation, it is entirely achievable. Here’s a guide to help you navigate the process:

Securing a mortgage as a self-employed professional can be more challenging than for traditional W-2 employees, but with the right preparation and documentation, it is entirely achievable. Here’s a guide to help you navigate the process:

The previous week had the Federal Reserve making their first rate decision since the Trump administration had taken office. With many uncertainties about the current direction of things, the Federal Reserve had decided there would not be any change necessary to the current rates. Stating that the current inflation and economic conditions have largely been a result of the Trump administration’s policies on tariffs. Chairman Powell has been strongly dovish at this point, stating they would need to “see how things actually work out.” There were a slew of other minor data releases but none were far reaching in their impact on the economy and current direction of things.

The previous week had the Federal Reserve making their first rate decision since the Trump administration had taken office. With many uncertainties about the current direction of things, the Federal Reserve had decided there would not be any change necessary to the current rates. Stating that the current inflation and economic conditions have largely been a result of the Trump administration’s policies on tariffs. Chairman Powell has been strongly dovish at this point, stating they would need to “see how things actually work out.” There were a slew of other minor data releases but none were far reaching in their impact on the economy and current direction of things. Purchasing a home in the U.S. as a non-U.S. citizen is entirely possible, but the process comes with unique requirements and considerations. Whether you are a permanent resident, temporary visa holder, or foreign national, understanding the available mortgage options can help you navigate the path to homeownership successfully.

Purchasing a home in the U.S. as a non-U.S. citizen is entirely possible, but the process comes with unique requirements and considerations. Whether you are a permanent resident, temporary visa holder, or foreign national, understanding the available mortgage options can help you navigate the path to homeownership successfully. For homeowners facing temporary financial hardship, mortgage payment deferral programs can provide much-needed relief. These programs allow borrowers to pause or reduce their monthly mortgage payments for a specific period, helping them avoid foreclosure while stabilizing their finances.

For homeowners facing temporary financial hardship, mortgage payment deferral programs can provide much-needed relief. These programs allow borrowers to pause or reduce their monthly mortgage payments for a specific period, helping them avoid foreclosure while stabilizing their finances.