Life is full of unexpected expenses, from medical bills to car repairs and even job loss. Having an emergency fund in place can help protect you from financial stress and prevent you from relying on high-interest loans or credit cards. If you don’t already have one, now is the perfect time to start building your safety net.

Life is full of unexpected expenses, from medical bills to car repairs and even job loss. Having an emergency fund in place can help protect you from financial stress and prevent you from relying on high-interest loans or credit cards. If you don’t already have one, now is the perfect time to start building your safety net.

Why an Emergency Fund Matters

An emergency fund is a dedicated savings account meant to cover unexpected expenses such as:

- Major home or appliance repairs

- Car repairs or replacements

- Unexpected medical bills

- Job loss or reduced income

Without savings, many people turn to credit cards or loans, which can lead to more debt. An emergency fund provides peace of mind and financial stability when life throws a curveball.

How Much Should You Save?

Financial experts recommend saving three to six months’ worth of essential living expenses. This amount ensures you have enough funds to cover necessities if you lose your income or face a major expense. If that goal seems overwhelming, start small—any savings is better than none. The key is to begin and build over time.

Steps to Build Your Emergency Fund

1) Determine Your Savings Goal

To figure out how much you need, calculate your monthly expenses, including:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries

- Insurance (health, home, auto)

- Car payments and transportation costs

- Credit card or loan payments

- Childcare or medical costs

Multiply that total by three to determine a three-month emergency fund goal, or by six for a more secure six-month fund.

2) Set Up Automatic Deposits

One of the easiest ways to save is to automate the process. Set up an automatic transfer from your paycheck or checking account into a separate savings account. This ensures consistency and removes the temptation to spend the money elsewhere.

3) Save Small Amounts Consistently

Even small contributions add up over time. Simple ways to save include:

- Rounding up purchases and transferring the spare change into savings

- Setting aside a percentage of each paycheck

- Cutting back on non-essential expenses and redirecting that money to your emergency fund

4) Use Unexpected Money Wisely

If you receive a tax refund, work bonus, or other unexpected cash, consider saving a portion of it. Large lump sums can give your emergency fund a significant boost.

5) Keep Your Fund Separate and Untouched

It’s important to distinguish between emergency savings and other savings goals. While it may be tempting to dip into your fund for a vacation or new gadget, keep this money reserved strictly for true emergencies. If possible, open a separate account to prevent easy access.

Building an emergency fund takes time and discipline, but even small steps will help you create financial security. By consistently saving, automating deposits, and keeping your funds for true emergencies, you can protect yourself from unexpected financial stress and gain greater peace of mind.

Buying your first home is an exciting milestone, but navigating the mortgage process can feel overwhelming. With so many loan options available, it is important to choose one that best suits your financial situation and long-term goals. Here are three of the most popular home loan programs that first-time buyers should consider.

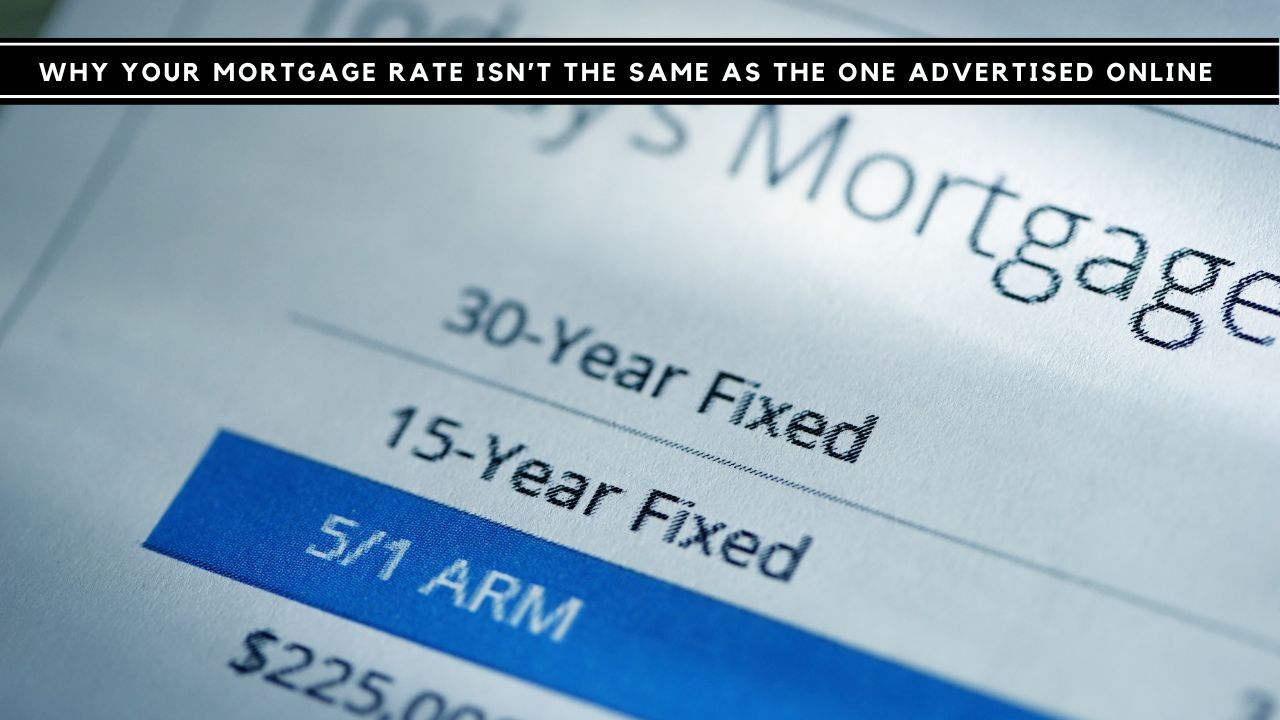

Buying your first home is an exciting milestone, but navigating the mortgage process can feel overwhelming. With so many loan options available, it is important to choose one that best suits your financial situation and long-term goals. Here are three of the most popular home loan programs that first-time buyers should consider. Shopping for a mortgage can be exciting, but it can also be confusing when you see a low advertised rate online, only to be quoted a different rate when you apply. While this can be frustrating, there are several reasons why your actual mortgage rate may differ from what you initially expected. The good news is that understanding these factors can help you make informed decisions and secure the best possible rate for your financial situation.

Shopping for a mortgage can be exciting, but it can also be confusing when you see a low advertised rate online, only to be quoted a different rate when you apply. While this can be frustrating, there are several reasons why your actual mortgage rate may differ from what you initially expected. The good news is that understanding these factors can help you make informed decisions and secure the best possible rate for your financial situation. With rising home prices and strict lending requirements, many aspiring homeowners are looking for creative ways to strengthen their mortgage applications. One potential game-changer? Renting out a room on Airbnb or another short-term rental platform. This additional income stream could help you qualify for a mortgage and make homeownership more affordable.

With rising home prices and strict lending requirements, many aspiring homeowners are looking for creative ways to strengthen their mortgage applications. One potential game-changer? Renting out a room on Airbnb or another short-term rental platform. This additional income stream could help you qualify for a mortgage and make homeownership more affordable. When applying for a mortgage, you expect lenders to scrutinize your income, credit score, and debt-to-income ratio. But did you know that your Netflix subscription—or any other recurring expense—could play a role in your approval?

When applying for a mortgage, you expect lenders to scrutinize your income, credit score, and debt-to-income ratio. But did you know that your Netflix subscription—or any other recurring expense—could play a role in your approval?

When you’re thinking about buying a home, you may hear a lot about mortgage rates going up or down. But have you ever wondered what causes these changes? One of the biggest influences on mortgage rates is the Federal Reserve, often called “the Fed.” While the Fed doesn’t set mortgage rates directly, its policies play a major role in how much you’ll pay for your home loan. Let’s break it down in simple terms:

When you’re thinking about buying a home, you may hear a lot about mortgage rates going up or down. But have you ever wondered what causes these changes? One of the biggest influences on mortgage rates is the Federal Reserve, often called “the Fed.” While the Fed doesn’t set mortgage rates directly, its policies play a major role in how much you’ll pay for your home loan. Let’s break it down in simple terms: Effective communication between mortgage originators and clients is essential in ensuring a smooth, stress-free home financing process. Purchasing a home is one of the biggest financial decisions a person can make, and navigating the mortgage process can be overwhelming. Strong communication helps clients understand their options, stay informed, and ultimately secure the best loan for their needs.

Effective communication between mortgage originators and clients is essential in ensuring a smooth, stress-free home financing process. Purchasing a home is one of the biggest financial decisions a person can make, and navigating the mortgage process can be overwhelming. Strong communication helps clients understand their options, stay informed, and ultimately secure the best loan for their needs. When shopping for a home, securing mortgage pre-approval is one of the most important steps you can take. Not only does it show sellers that you are a serious buyer, but it also gives you a clearer picture of your budget and financing options. However, many homebuyers do not realize that mortgage pre-approval can be leveraged in multiple ways to maximize their home search and negotiation power.

When shopping for a home, securing mortgage pre-approval is one of the most important steps you can take. Not only does it show sellers that you are a serious buyer, but it also gives you a clearer picture of your budget and financing options. However, many homebuyers do not realize that mortgage pre-approval can be leveraged in multiple ways to maximize their home search and negotiation power.