The Ultimate Guide to Choosing the Right Mortgage Lender

The Ultimate Guide to Choosing the Right Mortgage Lender

When you’re buying a home, choosing the right mortgage lender is one of the most critical decisions you’ll make. Your lender impacts your interest rates, fees, and overall homebuying experience. With so many options available, how do you make the best choice?

This ultimate guide will walk you through the key factors to consider, questions to ask, and tips to ensure you partner with a lender who meets your needs.

1. Understand Your Mortgage Options to Choose the Best Lender

Before choosing a lender, it’s important to understand the types of mortgages available. Different lenders may specialize in specific loan products, so knowing what fits your financial situation can narrow down your choices.

Explore Common Mortgage Types for the Best Fit:

- Conventional Loans: Require good credit and a stable income.

- FHA Loans: Great for first-time buyers with lower credit scores.

- VA Loans: Designed for veterans and active-duty military members.

- USDA Loans: Ideal for buyers in rural areas with moderate incomes.

Research these options and determine which aligns with your goals.

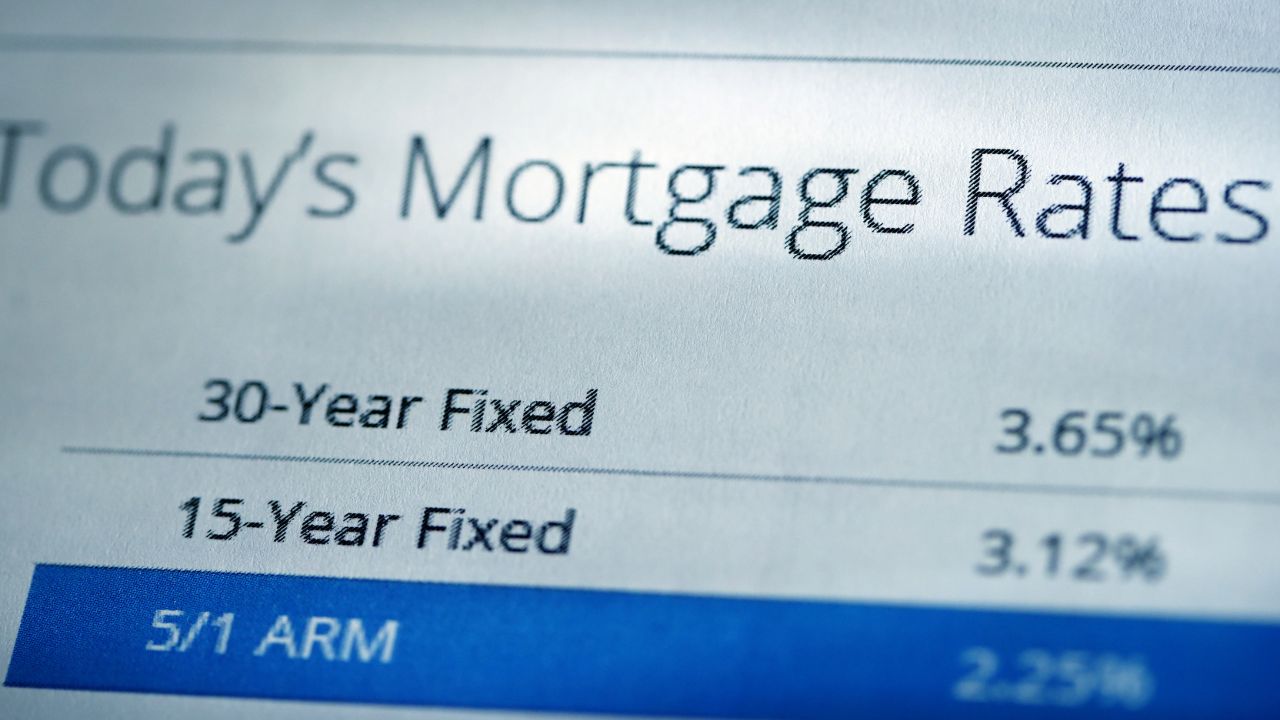

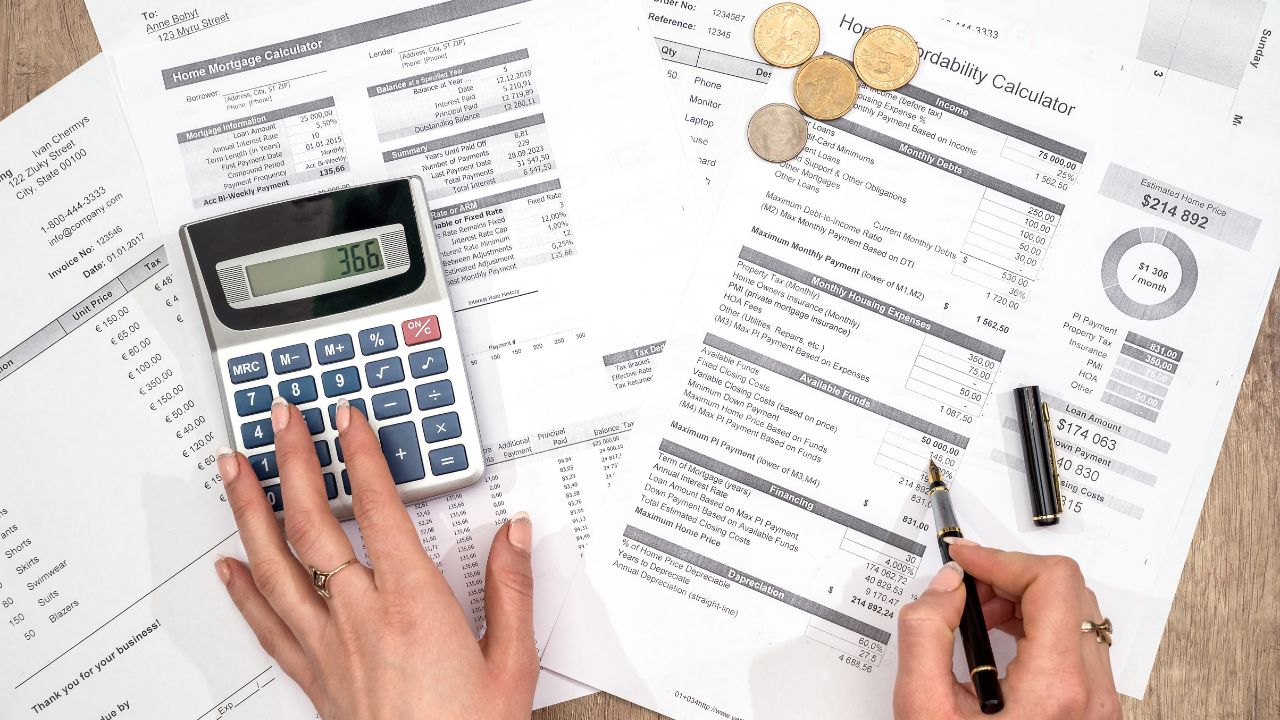

2. Compare Mortgage Interest Rates and Lender Fees

Your mortgage interest rate can significantly affect how much you pay over the life of your loan. While rates vary between lenders, they also depend on factors like your credit score and down payment.

Key Factors to Compare Among Lenders:

- Interest Rates: Request rate quotes from multiple lenders.

- Closing Costs: Lenders may charge fees like origination fees, appraisal fees, and more. Ask for a detailed breakdown.

- Points: Some lenders offer discount points to lower your interest rate, but these come with an upfront cost.

Use tools like a mortgage calculator to see how different rates and fees impact your monthly payment.

3. Evaluate Mortgage Lender Customer Service

A mortgage is a long-term commitment, and you’ll likely work with your lender for years. Great customer service can make the process smoother and less stressful.

How to Assess Lender Customer Service:

- Read Reviews: Check online reviews to learn about other buyers’ experiences.

- Ask for Referrals: Friends, family, and real estate agents can recommend trusted lenders.

- Communication Style: Choose a lender who is responsive and explains complex terms clearly.

4. Check for Preapproval Options

Getting preapproved for a mortgage is a critical step in the homebuying process. Preapproval shows sellers you’re a serious buyer and gives you a clear idea of your budget.

What to Look for in Preapproval:

- A detailed review of your credit, income, and assets.

- A preapproval letter you can provide to sellers.

- Clear communication about how much you qualify to borrow and the terms involved.

5. Ask the Right Questions

When you meet with potential lenders, asking the right questions can help you compare options and understand your loan.

Key Questions to Ask:

- What types of loans do you offer?

- What are the current interest rates and fees?

- Are there any special programs for first-time buyers?

- How long does it take to close on a loan?

- Can I lock in my interest rate?

6. Compare Local Lenders and Big Banks for Your Mortgage

Deciding between a local lender and a big bank often depends on your priorities.

Benefits of Choosing Local Mortgage Lenders:

Tend to offer personalized service and local expertise.

Advantages of Big Banks for Mortgages:

Often have competitive rates and a wide range of loan options.

Evaluate which aligns better with your needs and preferences.

7. Look for Special Programs and Discounts

Many lenders offer programs designed to help specific buyers, such as first-time homebuyers or those in specific professions. These can include lower down payments, reduced interest rates, or assistance with closing costs.

Examples:

- State-sponsored first-time homebuyer programs.

- Down payment assistance programs.

- Employer or union benefits.

Conclusion

Choosing the right mortgage lender can feel overwhelming, but taking the time to research, compare, and ask the right questions will pay off. The right lender can save you money, reduce stress, and help you achieve your homeownership dreams.

If you’re ready to start the process or have questions about finding the right lender, let’s connect! I’m here to guide you every step of the way.

📞 Contact Coleen TeBockhorst at 612-701-8512 🌐 Visit: Bay Equity Home Loans – Coleen TeBockhorst Facebook: Coleen TeBockhorst

Refinancing your mortgage can be a strategic financial decision, enabling you to save money, access home equity, or adjust your loan terms to better suit your current financial situation. Here’s a detailed guide to help you understand the process and determine if refinancing is the right move for you.

Refinancing your mortgage can be a strategic financial decision, enabling you to save money, access home equity, or adjust your loan terms to better suit your current financial situation. Here’s a detailed guide to help you understand the process and determine if refinancing is the right move for you. Have you ever calculated how much rent you’ve paid over the years? It’s a staggering number. According to studies, the average American spends between $133,000 and $155,000 on rent in just six to seven years. Let’s break that down and explore what it means for your financial future—and how you might be able to change that narrative.

Have you ever calculated how much rent you’ve paid over the years? It’s a staggering number. According to studies, the average American spends between $133,000 and $155,000 on rent in just six to seven years. Let’s break that down and explore what it means for your financial future—and how you might be able to change that narrative. Dreaming of owning a home? Preparing your finances for a mortgage is key to making that dream a reality. Here’s how to get started:

Dreaming of owning a home? Preparing your finances for a mortgage is key to making that dream a reality. Here’s how to get started:

Mortgage rates play a significant role in determining how much home you can afford. These rates influence the cost of borrowing money for your mortgage, which directly impacts your monthly payment and, ultimately, your home buying power.

Mortgage rates play a significant role in determining how much home you can afford. These rates influence the cost of borrowing money for your mortgage, which directly impacts your monthly payment and, ultimately, your home buying power. For many potential homeowners, the dream of buying a house can feel out of reach, especially when saving for a large down payment or dealing with credit challenges. That’s where FHA loans come in. Backed by the Federal Housing Administration, these loans have become a go-to option for first-time homebuyers and others looking for accessible and flexible financing options.

For many potential homeowners, the dream of buying a house can feel out of reach, especially when saving for a large down payment or dealing with credit challenges. That’s where FHA loans come in. Backed by the Federal Housing Administration, these loans have become a go-to option for first-time homebuyers and others looking for accessible and flexible financing options.

When you begin the exciting journey toward homeownership, understanding the financial aspects is vital. A key document in this process is the Loan Estimate. Provided by lenders when you apply for a mortgage, the Loan Estimate is your guide to deciphering the terms of your loan. Learning how to read and analyze this document is a significant step in making informed decisions about your home financing.

When you begin the exciting journey toward homeownership, understanding the financial aspects is vital. A key document in this process is the Loan Estimate. Provided by lenders when you apply for a mortgage, the Loan Estimate is your guide to deciphering the terms of your loan. Learning how to read and analyze this document is a significant step in making informed decisions about your home financing. When you’re in the market for a home loan, you’ll likely come across terms like “mortgage broker” and “mortgage originator.” While these professionals play critical roles in helping you secure financing, their responsibilities and how they serve you differ significantly. Understanding these distinctions can empower you to make informed decisions during your home-buying journey.

When you’re in the market for a home loan, you’ll likely come across terms like “mortgage broker” and “mortgage originator.” While these professionals play critical roles in helping you secure financing, their responsibilities and how they serve you differ significantly. Understanding these distinctions can empower you to make informed decisions during your home-buying journey.