Finding a new home loan can seem challenging, but if you take the proper steps before you start applying for loans, you’ll have no difficulty finding a mortgage that works for you and a lender that would love to have you as a borrower. Shopping for a mortgage isn’t like shopping for a couch, and there’s a lot that goes into the process.

Finding a new home loan can seem challenging, but if you take the proper steps before you start applying for loans, you’ll have no difficulty finding a mortgage that works for you and a lender that would love to have you as a borrower. Shopping for a mortgage isn’t like shopping for a couch, and there’s a lot that goes into the process.

So how can you shop for your new home loan in a way that saves you time and gets you the best loan for your needs? Here’s what you need to know.

Research Loan Types

A lot of home buyers, especially first-time buyers make the mistake of not doing their research and not asking enough questions. A fixed-rate mortgage isn’t right for every homebuyer. Neither is an adjustable-rate mortgage. If you plan to stay, put in a home to raise a family, you might consider a 30-year loan.

Conversely, if you’re moving in 10 years or less, an adjustable-rate mortgage, or ARM, could better suit you. It’s advised that you research loan types then prepare a list of questions to ask your mortgage agent to ensure you select the loan that’s best for you.

Get Pre-Qualified Before You Start Looking

It can be tempting to start looking for mortgages online and start seeing what kinds of rates and limits you can afford, but if you start your mortgage hunt with Internet window-shopping, you may end up sorely disappointed. A pre-qualification is a vital first step that can help you to find the mortgage that works best for you. With a pre-qualification, you’ll have a good idea of what you can reasonably afford to spend on a home, so you won’t waste time viewing homes that are outside of your price range.

Hold Off On Major Life Changes Until You Have Your Mortgage

Once you’ve been pre-qualified and pre-approved, the next step is the approval process, the part of the process where the lender you’ve chosen evaluates your application and decides whether or not to lend to you. One mistake that a lot of homebuyers make is allowing significant changes in their income to happen during the approval process. If you quit your job to start a business, or if you go down to part-time hours so you can spend more time with the kids, your lender will need to start the approval process again with your new financial information in mind, so hold off on any big changes until you’ve been approved.

Finding a new home loan can seem like a challenge, but a qualified mortgage advisor can help. Contact your local mortgage professional to learn more.

Co-signing a car loan may seem like a small favor for a family member or friend, but many homebuyers do not realize how much it affects their own mortgage approval. Even if you never drive the car, never make a payment, and never see the vehicle, the loan becomes legally and financially tied to you. Understanding how co-signing affects your credit, your debt, and your loan options can help you protect your mortgage eligibility.

Co-signing a car loan may seem like a small favor for a family member or friend, but many homebuyers do not realize how much it affects their own mortgage approval. Even if you never drive the car, never make a payment, and never see the vehicle, the loan becomes legally and financially tied to you. Understanding how co-signing affects your credit, your debt, and your loan options can help you protect your mortgage eligibility. Starting your career is an exciting milestone, and for many recent graduates, the idea of becoming a homeowner feels closer than ever. While student loans, new job transitions, and building credit can make the mortgage process feel overwhelming, you have more options and advantages than you may realize. With the right preparation, you can move toward homeownership confidently and avoid common first-time buyer mistakes.

Starting your career is an exciting milestone, and for many recent graduates, the idea of becoming a homeowner feels closer than ever. While student loans, new job transitions, and building credit can make the mortgage process feel overwhelming, you have more options and advantages than you may realize. With the right preparation, you can move toward homeownership confidently and avoid common first-time buyer mistakes.

The Federal Reserve’s preferred inflation indicator — the Personal Consumption Expenditures (PCE) Index — released under delayed conditions, but it was within expectations. Next week will be another Federal Reserve Rate Decision, and it is expected that the Federal Reserve will reduce rates at least one more time. The optimism among the broader market has been showing that multiple sectors that seem unphased by the administrative decisions and current political climate.

The Federal Reserve’s preferred inflation indicator — the Personal Consumption Expenditures (PCE) Index — released under delayed conditions, but it was within expectations. Next week will be another Federal Reserve Rate Decision, and it is expected that the Federal Reserve will reduce rates at least one more time. The optimism among the broader market has been showing that multiple sectors that seem unphased by the administrative decisions and current political climate.  Divorce or separation is a challenging time, and amidst the emotional and logistical complexities, handling mortgage issues can add another layer of stress. For many couples, their home represents not just a financial investment but a symbol of stability and security. However, when relationships break down, decisions about homeownership become crucial. Here is some guidance on how to navigate mortgages during a divorce or separation.

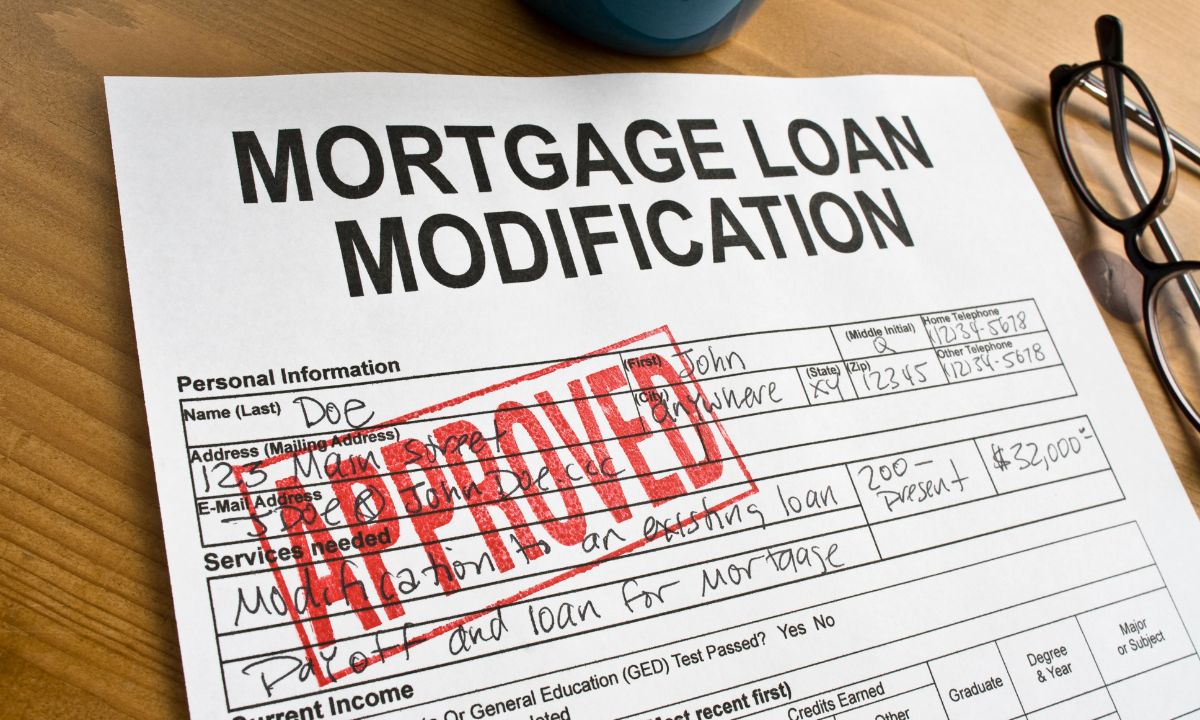

Divorce or separation is a challenging time, and amidst the emotional and logistical complexities, handling mortgage issues can add another layer of stress. For many couples, their home represents not just a financial investment but a symbol of stability and security. However, when relationships break down, decisions about homeownership become crucial. Here is some guidance on how to navigate mortgages during a divorce or separation. In times of financial hardship, such as job loss, medical emergencies, or economic downturns, homeowners may find it challenging to keep up with their mortgage payments. When facing such difficulties, understanding options like mortgage forbearance and loan modification can be crucial for maintaining stability and avoiding foreclosure. Let’s discuss what homeowners need to know about mortgage forbearance and loan modification, including their differences, implications, and how to navigate these options effectively.

In times of financial hardship, such as job loss, medical emergencies, or economic downturns, homeowners may find it challenging to keep up with their mortgage payments. When facing such difficulties, understanding options like mortgage forbearance and loan modification can be crucial for maintaining stability and avoiding foreclosure. Let’s discuss what homeowners need to know about mortgage forbearance and loan modification, including their differences, implications, and how to navigate these options effectively. Are you in the market for a new home? Have you considered the allure of a fixer-upper? While the idea of purchasing a home that needs a bit of TLC might seem daunting at first, numerous benefits come with this type of investment. We will plunge into the exciting world of fixer-uppers and uncover why they might just be the perfect choice for you.

Are you in the market for a new home? Have you considered the allure of a fixer-upper? While the idea of purchasing a home that needs a bit of TLC might seem daunting at first, numerous benefits come with this type of investment. We will plunge into the exciting world of fixer-uppers and uncover why they might just be the perfect choice for you. Inflation reports have shown their cards, and they have come in line with expectations. These newer reports rely on less data from sources overall, which is why the PCE Index remains the Federal Reserve’s preferred inflation indicator—and that distinction is even more relevant now.

Inflation reports have shown their cards, and they have come in line with expectations. These newer reports rely on less data from sources overall, which is why the PCE Index remains the Federal Reserve’s preferred inflation indicator—and that distinction is even more relevant now. Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?

Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?