Buying a home is more than a place to live, it is a path to financial growth, every mortgage payment builds equity, giving homeowners a valuable asset over time, unlike renting where monthly payments go to a landlord, homeowners are investing in their future, with the right mortgage strategy, owning a home can be one of the smartest financial moves you make.

Buying a home is more than a place to live, it is a path to financial growth, every mortgage payment builds equity, giving homeowners a valuable asset over time, unlike renting where monthly payments go to a landlord, homeowners are investing in their future, with the right mortgage strategy, owning a home can be one of the smartest financial moves you make.

Stability and Freedom

Homeownership offers stability and freedom to create a space that truly reflects your lifestyle, you can renovate, decorate, and plan for the long term without restrictions, for families, it provides a secure foundation, a community to grow in, and the ability to put down roots, knowing your home is yours creates peace of mind that renting cannot provide

Tax Benefits and Financial Incentives

Owning a home comes with valuable financial perks, mortgage interest and property taxes are often tax-deductible, which can reduce your overall financial burden, programs like first-time homebuyer incentives or low down payment options make homeownership even more accessible, with these tools, buying a home is not just a dream, it is an achievable step toward long-term wealth.

Flexibility in Today’s Market

Even in changing markets, smart mortgage options provide flexibility, fixed-rate mortgages offer predictable payments, while adjustable-rate and other specialized loans can be tailored to fit your financial goals, mortgage originators are here to help you find the best solution, guiding you through pre-approval, closing, and beyond, with expert guidance, homeownership remains an attainable and rewarding goal.

Long-Term Investment Potential

Homes historically appreciate over time, making them one of the most reliable ways to grow wealth. By carefully choosing a property and mortgage plan, homeowners can build equity, increase net worth, and create opportunities for rental income or future investment properties. With planning and support, your home becomes a steppingstone to financial security.

Making the Dream Your Reality

Homeownership is not just a nostalgic dream, it is a practical, achievable goal, with the right mortgage, you can enjoy stability, build wealth, and create a home that supports your lifestyle, working with a knowledgeable mortgage originator ensures you find a plan that fits your budget, maximizes your benefits, and makes homeownership a positive, empowering experience.

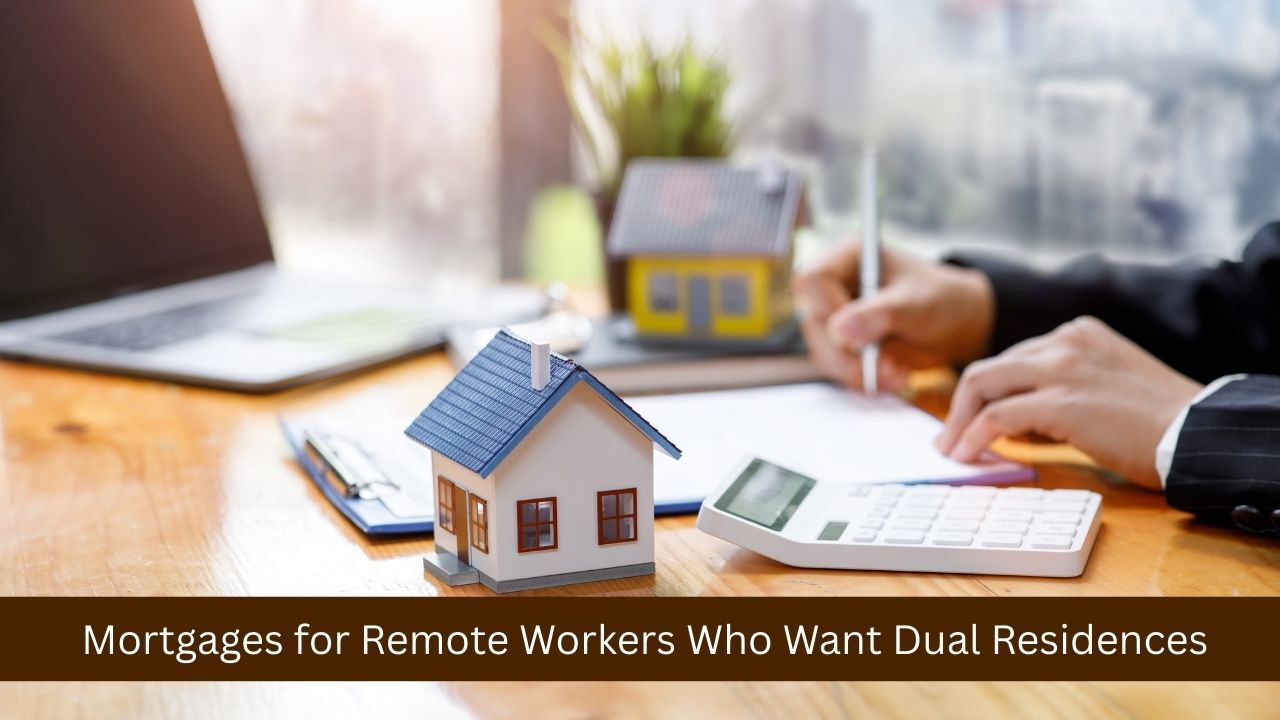

Remote work has transformed the way people live and plan their financial futures. Instead of being tied to one city, many professionals now choose to split their time between two homes. Some want the excitement of an urban condo while keeping a peaceful retreat in the mountains or at the beach. Others need to balance family life in one state with work opportunities in another. As this trend grows, understanding mortgage options for dual residences has become essential.

Remote work has transformed the way people live and plan their financial futures. Instead of being tied to one city, many professionals now choose to split their time between two homes. Some want the excitement of an urban condo while keeping a peaceful retreat in the mountains or at the beach. Others need to balance family life in one state with work opportunities in another. As this trend grows, understanding mortgage options for dual residences has become essential.

When it comes to qualifying for a mortgage, your income plays a key role in determining how much you can borrow. For many buyers, especially those interested in investment properties or who plan to rent out part of their home, the question is whether rental income can be counted toward their mortgage qualification. The good news is that in many cases, rental income can help, but there are specific rules and documentation requirements you will need to meet.

When it comes to qualifying for a mortgage, your income plays a key role in determining how much you can borrow. For many buyers, especially those interested in investment properties or who plan to rent out part of their home, the question is whether rental income can be counted toward their mortgage qualification. The good news is that in many cases, rental income can help, but there are specific rules and documentation requirements you will need to meet. Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable.

Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable. Many potential homebuyers worry that carrying credit card debt will prevent them from qualifying for a mortgage. While it is true that lenders carefully evaluate your financial profile, having credit card balances does not automatically disqualify you. By understanding how lenders view debt, taking strategic steps to improve your application, and choosing the right mortgage program, you can still achieve your goal of homeownership.

Many potential homebuyers worry that carrying credit card debt will prevent them from qualifying for a mortgage. While it is true that lenders carefully evaluate your financial profile, having credit card balances does not automatically disqualify you. By understanding how lenders view debt, taking strategic steps to improve your application, and choosing the right mortgage program, you can still achieve your goal of homeownership. Buying a fixer-upper can be an exciting way to get into a desirable neighborhood at a lower price point, while also creating a home that reflects your style and needs. However, financing a property that needs significant repairs can be challenging if you are only looking at traditional mortgage products. The good news is there are several mortgage options designed specifically for buyers who are ready to take on a renovation project. Understanding these options can help you choose the right path to turn a home with potential into your dream property.

Buying a fixer-upper can be an exciting way to get into a desirable neighborhood at a lower price point, while also creating a home that reflects your style and needs. However, financing a property that needs significant repairs can be challenging if you are only looking at traditional mortgage products. The good news is there are several mortgage options designed specifically for buyers who are ready to take on a renovation project. Understanding these options can help you choose the right path to turn a home with potential into your dream property.

When purchasing a home, buyers typically assume a new mortgage loan. However, in some situations, a buyer may opt to assume the seller’s existing mortgage. Known as a mortgage assumption, this process allows the buyer to take over the terms and payments of the seller’s current loan. While mortgage assumptions can offer benefits, they also come with certain drawbacks. Understanding the pros and cons of mortgage assumptions can help you determine whether this option is right for you.

When purchasing a home, buyers typically assume a new mortgage loan. However, in some situations, a buyer may opt to assume the seller’s existing mortgage. Known as a mortgage assumption, this process allows the buyer to take over the terms and payments of the seller’s current loan. While mortgage assumptions can offer benefits, they also come with certain drawbacks. Understanding the pros and cons of mortgage assumptions can help you determine whether this option is right for you. Going through bankruptcy can be a challenging and stressful process. However, it s important to understand how bankruptcy may affect your ability to secure a mortgage in the future. Bankruptcy, whether Chapter 7 or Chapter 13, can significantly impact your credit score and financial history, both of which are critical factors when applying for a mortgage. Despite this, it’s possible to obtain a mortgage after bankruptcy, though the path may be a bit more complicated.

Going through bankruptcy can be a challenging and stressful process. However, it s important to understand how bankruptcy may affect your ability to secure a mortgage in the future. Bankruptcy, whether Chapter 7 or Chapter 13, can significantly impact your credit score and financial history, both of which are critical factors when applying for a mortgage. Despite this, it’s possible to obtain a mortgage after bankruptcy, though the path may be a bit more complicated.